Disclaimer: This article is for informational and personal educational purpose only, and is not in any shape or form a medical, legal or financial advice, neither it is sponsored by or affiliated with insurance or any company or business entity and cannot be a substitute of professional medical, legal or financial advice. All the posts are the results of thorough research and writer’s personal experience. Insurance policies vary widely; always consult with a medical, legal or licensed insurance professional before making any decisions on cancer or any other insurance.

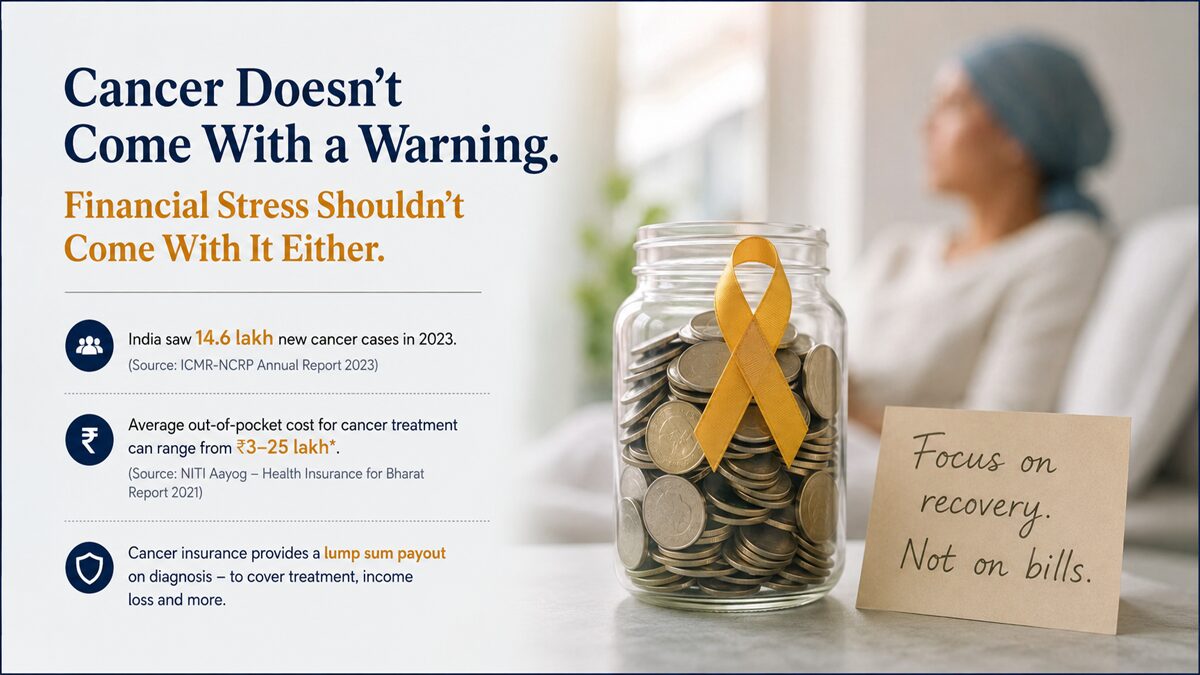

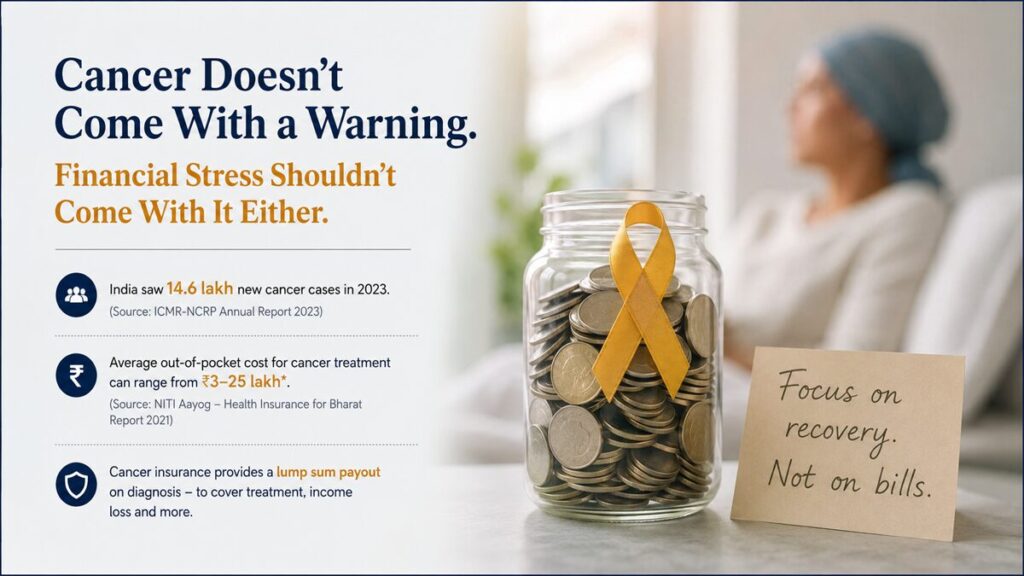

Cancer suddenly takes more than health — it takes time, income, and the quiet security of a family’s future. For many Indians, the clinical bills are just the start: long outpatient cycles, travel for specialist care, home modifications, and months without steady wages.

This is where cancer-specific insurance that pays large lump sums (and optional income payouts) becomes not just desirable, but transformational — a monetary firewall that buys time, choice, and access to the latest treatments.

Below is a focused, evidence-backed guide to why cash-payout and income-generation cancer plans matter, how they differ from regular health cover, why younger people often ignore them, and how timely purchase can unlock access to cutting-edge therapies — with references to two major Indian offerings (HDFC ERGO iCan, Aditya Birla Activ Secure, Star Health, Tata AIG, and LIC’s Cancer Cover).

Later on, after you read this article, you can read the next article What Type of Payout Method Should you Opt for Cancer Insurance: Understand With LIC’s Cancer Cover vs Aditya Birla’s Activ Secure Comparison where you can be clear about how would you want to receive payments at an unfortunate event of diagnosis of cancer.

Why lump-sum cancer payouts are not “just another policy”

Traditional health insurance typically reimburses hospital bills or offers cashless admission. That’s vital — but limited. Lump-sum cancer plans pay a fixed amount on confirmed diagnosis. That money is unrestricted: it can cover experimental drugs, travel to a specialist abroad, hire caregivers, replace lost income, or simply prevent forced liquidation of savings and investments. The flexibility is the policy’s strategic advantage.

Insurance providers explicitly position some products for this purpose, for example HDFC ERGO’s iCan is framed around comprehensive cancer treatments with cashless options and benefits geared to diagnosis-triggered payouts. HDFC ERGO Insurance and Aditya Birla’s Activ Secure Cancer which provides payouts upon diagnosis for different stages of cancer

The two payout models you must know

- Flat lump-sum on diagnosis (one-time payment). Ideal when immediate liquidity is needed — e.g., to buy targeted therapy not covered by standard hospital packages.

- Stage-based + income features. Some plans pay a fraction of the sum for early-stage detection and larger multiples for advanced stages; others add a monthly income benefit to replace salary during recovery.

Aditya Birla’s Activ Secure explicitly uses a stage-based model (50% for early or maximum of ₹10 Lakhs, 100% for major, 150% for advanced) — a structure that turns early detection into immediate, usable capital.

LIC’s role — a public-trust angle many miss

Most think only private insurers sell cancer riders. Not so: LIC also markets a dedicated “LIC’s Cancer Cover” (Plan 905/ UIN 512N314V03) that provides defined benefits for early and major stage cancers. Including LIC in the shortlist provides a government-trusted alternative for those who prefer conservative, regulated products.

Why these payouts matter for access to cutting-edge care

Cutting-edge oncology often means targeted oral agents like immunotherapies, India’s newest indigenously developed CAR T-cell therapy called NexCAR19, or novel clinical trials — options that may require to be borne out-of-pocket even with excellent hospitalization cover.

A lump-sum or enhanced stage payout lets families and individuals who wishes for the top of the class treatment decide on their options of treatment rather than be limited by what a standard bill will reimburse. HDFC ERGO’s iCan literature highlights coverage for advanced procedures and therapies beyond hospitalization — a clear signal that lump-sum style protection supports modern care pathways. HDFC ERGO Insurance

Some overlooked psychological and financial benefits

- Immediate liquidity = emotional breathing room. A lump-sum prevents frantic asset sales and reduces decision stress during a traumatic diagnosis.

- Household continuity. Income riders or monthly payouts substitute lost wages, protecting dependents.

- Choice of centre and treatment. Cash enables travel to specialist centres or trials that improve survival odds.

- Premium waiver on diagnosis. Some plans waive future premiums after payout — preserving future cover without additional cost.

Why young people postpone or ignore cancer cover (and why that’s risky)

- Optimism bias: “It won’t happen to me” is powerful — especially when budgets are tight and priorities skew to rent, EMIs, or SIPs.

2. Low perceived immediacy: Unlike term life or vehicle insurance, cancer feels abstract until it isn’t.

3. Misunderstanding of product role: Many conflate cancer cover with standard health insurance and miss that lump-sum payouts are a different utility.

4. Cost sensitivity: Younger people may choose cheaper incidental riders or delay buying at all.

This combination is dangerous because incidence patterns are shifting: national registries and peer-reviewed analyses show a rising fraction of cancers occurring in younger age bands in India, and incidence begins to climb in the early thirties for several common cancers (breast, oral, colorectal). Early purchase locks in insurability and lower premiums while risk factors are still manageable. Check Indian Journal of Medical Research

The single most important reason to buy early: insurability

Most cancer plans require medical underwriting and have waiting periods. Buying when you are healthy avoids exclusions and pre-existing clauses, preserves lower premiums, and secures the right to larger sum assureds.

When diagnosis strikes first, many find they are uninsurable or face long waiting periods — the opposite of what’s needed when time matters.

How to judge a payout-focused cancer plan (practical checklist)

- Payout structure: Lump-sum vs stage-based vs hybrid. Does it include extra top-ups for advanced therapy? (To get the idea, check Activ Secure brochure of Aditya Birla for stage multipliers)

- Sum assured size: For meaningful protection, prefer plans that let you pick ₹50L–₹1Cr+ for metropolitan care access.

- Waiting & survival period: Confirm the waiting period (often 90 days+) and survival period required to qualify for payout.

- Premium waiver on payout: This preserves future cover without further premium drain. (Check LIC’s cancer plan for example)

- Renewability & portability: Lifelong renewability and portability reduce future friction (HDFC ERGO iCan highlights life-long renewals). HDFC ERGO Insurance

- Claim settlement clarity: Read sample claim scenarios and check insurer reputation for cancer claims (Star/TATA pages often cite customer support and networks).

Realistic scenarios where cash payouts make the difference

- A 38-year-old executive diagnosed with an aggressive subtype chooses immunotherapy + targeted oral agent not fully covered by indemnity policies. A lump sum funds the therapy, reducing recurrence risk.

- A primary earner receives a monthly income payout for 12 months during treatment, covering mortgage and school fees and preventing ruinous debt.

- Early detection pays out a smaller lump sum; the family uses it to get second opinions and choose a higher success rated treatment centre — turning early payout into survival capital.

Shortlist of notable India Cancer Insurances

- HDFC ERGO — iCan Cancer Insurance: Cancer-focused product with cashless support, emphasis on advanced therapy coverage and life-long renewability. HDFC ERGO Insurance

- Aditya Birla — Activ Secure Cancer : Stage-based payouts (50%/100%/150%) and possible additional payouts on progression; good for those who value structured payouts by stage. Brochure details payout math.

- Star Health — Cancer Care Platinum: Standalone cancer policy with lump-sum diagnosis benefits and options for added supports; positioned for both diagnosis and treatment expenses.

- Tata AIG — Cancer-specific offerings: Family of cancer products with targeted plans (including specialized subtypes) and strong network reach. TATA AIG

- LIC — LIC’s Cancer Cover (Plan 905): A government-backed cancer plan providing defined benefits for early/major stages — useful for conservative buyers preferring LIC’s structure.

Actionable steps: What to Do next

- You need to decide the core need: Is it immediate liquidity (lump sum), income replacement (monthly payments), or both?

- Pick a target sum assured — think in terms of realistic modern oncology costs in major cities (₹50L–₹1Cr+ for advanced therapies).

- Compare 2–3 policies on: payout structure, waiting period, survival period, premium waiver, renewability, and claim references. Use official brochures and policy wordings to confirm exclusions.

- You should buy earlier rather than later. The cost of a policy in the 30s is measurably lower than in the 40s; underwriting is simpler; and the policy can deliver a decisive financial buffer if the unexpected occurs.

Finally

Cancer doesn’t announce itself. When it arrives, money should not be the gatekeeper to good care. For those who can afford a plan, a lump-sum or income-enabled cancer policy is less a luxury and more a strategic lifeline — purchase timing, sum chosen, and payout design determine whether it will act as a bridge to recovery or merely a line item on a creditor’s ledger.

Also read the next article What Type of Payout Method Should you Opt for Cancer Insurance: Understand With LIC’s Cancer Cover vs Aditya Birla’s Activ Secure Comparison