Disclaimer: This article is for informational and personal educational purpose only, and is not in any shape or form a medical, legal or financial advice, neither it is sponsored by or affiliated with insurance or any company or business entity and cannot be a substitute of professional medical, legal or financial advice. All the posts are the results of thorough research and writer’s personal experience. Insurance policies vary widely; always consult with a medical, legal or licensed insurance professional before making any decisions on cancer or any other insurance.

Most people think cancer insurance works in only one way: diagnosis happens, treatments starts, hospital bills arrive or insurer pays the hospital bills in cashless mode.

But modern cancer insurance has quietly evolved into two very different financial protection models.

One model focuses on large lump-sum payouts designed to absorb the exploding cost of advanced cancer treatments like immunotherapy, targeted drugs, and precision medicine. The other focuses on recurring income support, helping individuals and families survive financially when recovery becomes long, income stops, and daily life continues demanding stability.

If you haven’t read the article Cash Shield For Cancer: Why Do You Need It : India’s Urgent Overlooked Lifeline read it first, this will make you understand why do you even need a cancer insurance plan.

Both payout methods matter deeply — but for completely different reasons.

An individual or a family struggling to fund cutting-edge treatment may need immediate liquidity and aggressive payouts. Another individual or family may survive treatment itself, yet quietly collapse under years of interrupted income, EMIs, and financial uncertainty.

That is why comparing cancer insurance plans only through “sum insured” or premium amounts often misses the real picture entirely.

Among India’s most discussed cancer-focused plans, two products represent these contrasting philosophies particularly well:

These two plans are chosen just to explain the two ideas in general so that you can make intelligent decisions and no way they are presented here as the best of all. There could be better plans based on the two philosophies which better suits you, you do you.

Activ Secure is built more like an aggressive financial shield against rising oncology costs. LIC’s Cancer Cover, on the other hand, which also pays a lumpsum upon diagnosis of cancer, behaves more like a long-term household income stabilizer.

Both are strong.

Both can also feel insufficient — if purchased for the wrong purpose.

Understanding how these two payout philosophies work is where smarter cancer planning truly begins.

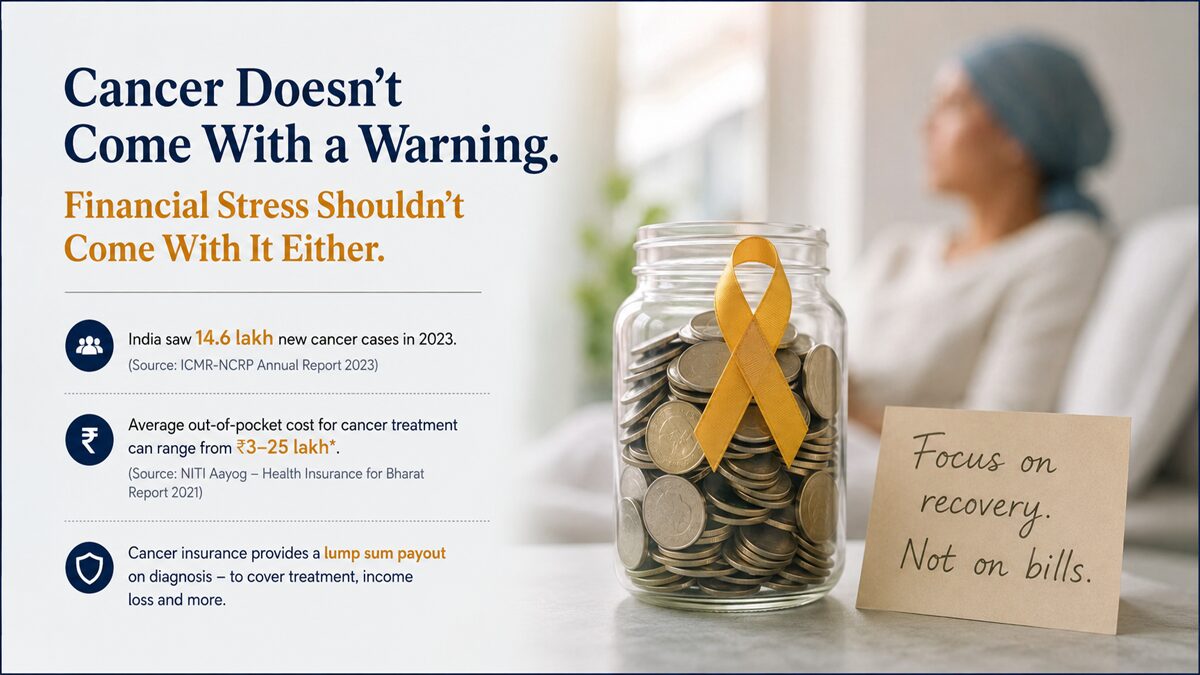

Cancer is No Longer Just a Hospital Expense

For years, health insurance was relatively simple. A patient got hospitalized, underwent surgery or treatment, and the insurer reimbursed the bill or settled it cashless.

While that system is still applicable and in fact most patients follow that system only, modern cancer care are evolving and cutting edge treatments are available for patients but with significant cost.

Today’s oncology ecosystem is vastly more complicated and significantly more expensive. Advanced cancer care increasingly involves immunotherapy, targeted precision medicine, genetic testing, long outpatient treatment cycles, recurring scans, imported biologic drugs, and rehabilitation expenses that continue far beyond hospitalization.

Many of these costs:

- Happen outside hospitals,

- Are only partially covered under traditional health insurance, or…

- Require immediate liquidity before reimbursement even begins.

This is precisely why cancer-specific payout plans have become far more relevant in recent years.

The strongest cancer insurance policies today are not merely “medical covers.”

They function more like financial survival systems during one of life’s most destabilizing crises.

Two Distinct Payout Methods: The Fundamental Difference Between LIC’s 905 Plan and Aditya Birla’s Activ Secure

At first glance, both policies appear similar. Both provide coverage for early-stage and major-stage cancers. Both waive future premiums under covered conditions. Both are designed to reduce financial strain after diagnosis.

But structurally, these plans are solving very different emotional and financial fears.

| Feature | Activ Secure Cancer Health Plan | LIC Cancer Cover |

| Core Philosophy | Aggressive stage-based protection | Long-term financial continuity |

| Best For | Advanced treatment inflation | Stable recurring family support |

| Payout Style | Up to 150% escalating payout | Lump sum + monthly income |

| Main Strength | Immediate liquidity | Predictable long-term support |

| Emotional Advantage | “Fight aggressively now” | “Keep the household stable” |

| Ideal Buyer | Younger urban earners | Conservative family-focused buyers |

These distinction changes everything.

Choosing between these two plans is not merely about comparing premiums or coverage amounts. It is about identifying the type of financial damage a family fears most.

Some worry about treatment inaccessibility. Others worry about income collapse. These plans address those concerns differently.

Activ Secure Cancer Plan: Built for the Era of Advanced Expensive Oncology

Aditya Birla’s Activ Secure Cancer Plan [The Brochure] feels designed around one uncomfortable modern reality:

Cancer treatment inflation is accelerating rapidly.

Advanced oncology is no longer limited to surgery, radiotherapy and chemotherapy. Precision medicine and modern biologics have transformed outcomes for many patients — but they have also dramatically increased costs.

This is where Activ Secure’s structure becomes particularly interesting.

Its standout feature is the escalating payout design:

- Early-stage cancer → up to 50% or 10 Lacs (whichever is less) payout

- Major-stage cancer → up to 100% payout

- Advanced-stage cancer → up to 150% payout, and..

- A claim free year results on a 10% cumulative bonus

That escalation does not seem to be just a marketing feature. It reflects the reality that treatment costs often explode as cancer becomes more advanced or who wish to go for advanced treatments from the early stage. But one must keep paying your regular premiums to stay covered for higher stages in case stagewise progression and pay outs.

A patient with aggressive-stage cancer may suddenly require:

- Imported targeted drugs,

- Prolonged immunotherapy,

- Advanced radiation cycles,

- Genomic profiling,

- Repeated imaging,

- Extended rehabilitation support.

Traditional reimbursement-only insurance models often struggle in these situations because treatment decisions cannot always wait for approvals, reimbursements or limited payment in a general health insurance (individual or family floater)

Activ Secure attempts to solve this problem through aggressive liquidity and designed specifically to tackle high cost cancer treatment.

Where Activ Secure Clearly Pulls Ahead

Advanced Treatment Readiness

This is arguably Activ Secure’s greatest strength.

Its higher-stage payout structure creates immediate financial flexibility at a time when treatment speed can matter enormously.

Families may suddenly need:

- Access to premium oncology centers,

- Newer targeted therapies,

- Second opinions from specialist hospitals,

- Or imported medicines not fully covered under standard plans.

In such situations, large payouts provide something extremely valuable: Luxury of a Choice

The policy behaves less like traditional insurance and more like a financial shock absorber designed for modern oncology inflation.

Better Protection Against Rising Medical Inflation

Cancer inflation is rising faster than general healthcare inflation.

Advanced cancer therapies today can easily cost ₹10–40 lakh or even more, especially when treatment involves immunotherapy, targeted therapy, CAR-T cell therapy, or prolonged precision oncology care. In India, immunotherapy alone can cost between ₹1.5 lakh to ₹4 lakh per cycle, while CAR-T therapies may range from ₹30 lakh to ₹60 lakh.

Targeted therapies in India are also becoming major cost drivers in oncology, with annual treatment expenses often reaching ₹5 lakh–₹25 lakh depending on the cancer type and duration of treatment.

A recent Tata Memorial Centre study further highlighted that newer immunotherapy drugs such as pembrolizumab and nivolumab remain financially out of reach for many Indian families due to their extremely high costs relative to average income levels.

That reality changes how cancer insurance should be evaluated.

Large lump-sum payouts create immediate liquidity, which can help individuals and families in :

- Avoiding distress borrowing,

- Continue treatment uninterrupted,

- Preserving investments,

- And reducing panic-driven financial decisions.

This becomes especially relevant for younger earners with long-term financial goals still in progress.

Why it is Even More Stronger for Younger Professionals

Younger urban earners often carry multiple financial responsibilities simultaneously like:

- Home loans,

- Dependent parents,

- Young children,

- Career growth pressure,

- And future wealth-building plans.

A major illness at this stage can financially derail decades of progress.

Activ Secure’s payout-heavy structure is particularly attractive for:

- Salaried professionals,

- Entrepreneurs,

- Dual-income households, and..

- Younger buyers seeking higher treatment flexibility.

The policy feels built for aggressive financial defense.

Where Activ Secure Feels Less Dominant

Despite its strengths, Activ Secure is not unbeatable.

Its design prioritizes:

- Immediate large payouts,

- Treatment readiness,

- And escalating financial protection.

But what happens after treatment?

What if survival improves — but earning capacity remains reduced for years?

That is precisely where LIC enters the conversation.

LIC’s Cancer Cover: Built as an Income Engine in Crisis

LIC’s Cancer Cover [Brochure] approaches cancer protection from a completely different angle.

It is less aggressive in branding. Less focused on dramatic payout escalation. Less modern in presentation.

But financially, it offers something emotionally powerful:

Monthly income continuity

The policy attempts to create financial continuity across different phases of diagnosis and recovery.

Under the policy structure outlined in the official brochure:

Early Stage Cancer Benefits

- Lump Sum Benefit: 25% of Applicable Sum Insured payable on first admissible diagnosis

- Premium Waiver Benefit: Premiums for the next 3 policy years or remaining policy term (whichever is lower) are waived

Major Stage Cancer Benefits

- Lump Sum Benefit: 100% of Applicable Sum Insured payable, after adjusting any earlier Early Stage Cancer claims

- Income Benefit: 1% of Applicable Sum Insured paid every month for the next 10 years to the patient or family, irrespective of survival of the patient or policy term expiry

- Premium Waiver Benefit: All future premiums waived after major-stage admissible diagnosis

That changes the emotional architecture of the policy entirely.

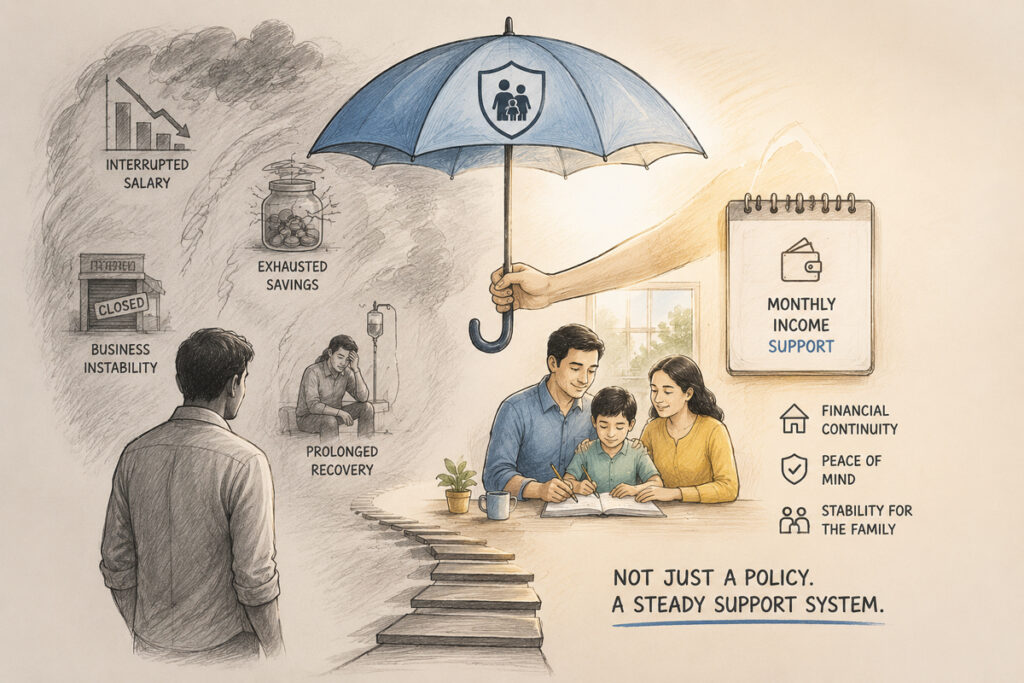

Instead of functioning only as a treatment-funding mechanism, LIC attempts to support households through both immediate medical stress and long-term financial uncertainty. The policy recognizes that cancer recovery often extends far beyond hospitalization, where interrupted income, reduced work capacity, EMIs, and daily household expenses continue even after treatment slows down.

For families dependent on one primary earner, the recurring monthly income component can feel especially reassuring because it creates predictable cashflow support during prolonged recovery periods. Rather than focusing purely on aggressive treatment liquidity, LIC’s structure leans more toward stability, continuity, and long-term household financial support.

Why LIC’s Cancer Cover Feels Emotionally Different

Many cancer battles are not lost inside hospitals.

They are lost slowly through:

- Interrupted salaries,

- Exhausted savings,

- Business instability, and…

- Prolonged recovery periods after treatment.

LIC’s recurring monthly income structure quietly addresses this emotional uncertainty. Rather than focusing only on aggressive treatment-stage payouts, the policy focuses on helping individuals and families maintain financial continuity while life gradually returns to normal.

That predictability can become deeply valuable during recovery, especially for conservative middle-class households, sole breadwinners, conservative financial planners, families dependent on one steady income source and families seeking long-term stability rather than only large immediate payouts.

In such situations, recurring monthly income can become more valuable than a single aggressive payout.

Emotional Predictability

Many Indian families fear one thing more than hospital bills:

Questions begin appearing immediately after diagnosis:

- How long will income stop?

- What happens to EMIs?

- What about children’s education?

- What if recovery takes years?

LIC’s recurring income structure directly addresses this emotional uncertainty.

That stability is often underestimated during policy comparisons.

Strong Premium Waiver Support

Cancer treatment frequently disrupts financial discipline:

- SIPs stop,

- Investments shrink,

- Savings get liquidated, and

- Policy premiums lapse.

LIC’s waiver structure helps preserve continuity precisely when households become financially vulnerable.

This may appear like a small feature initially, but during prolonged illness, it becomes deeply important.

But is LIC’s Cancer Cover Enough for Advanced Modern

Treatments?

This is where the comparison becomes more nuanced.

Income-focused cancer plans can sometimes feel comparatively conservative when viewed against the

rapidly rising cost of modern cancer care. These policies are generally structured more around long-term household financial continuity than aggressively maximizing treatment-stage liquidity.

While recurring income benefits, lump-sum payouts, and premium waivers can provide meaningful long-term support, such structures may not always feel fully optimized for very high treatment inflation or expensive advanced-care decisions that require immediate large liquidity.

These policies are designed more toward:

- Protecting household stability,

- Supporting long recovery phases,

- Maintaining predictable cashflow, and..

- Reducing financial stress caused by interrupted income.

Not necessarily toward exploding modern treatment costs.

That does not make LIC weak.

It simply means the policy is solving a different kind of financial problem.

Which Policy Wins in Real-Life Situations?

Scenario 1: Younger Urban Professional Seeking Advanced Treatment

For younger professionals pursuing:

- Immunotherapy,

- Targeted medicine,

- Imported drugs, or

- Premium oncology hospitals,

- Any new advanced treatments

Treatment flexibility matters more than recurring income.

In these situations, higher-stage payouts become extremely valuable, the winner here is Activ Secure

Scenario 2: Sole Breadwinner Supporting a Family

When a family depends heavily on one income source, recurring monthly support can become emotionally and financially stabilizing.

This becomes especially important if:

- Recovery is prolonged,

- Earning capacity declines, or

- Treatment interruptions affect career continuity.

Lic’s Cancer Cover is more suitable here.

Scenario 3: Future-Proofing Against Oncology Inflation

Cancer treatment inflation is rising rapidly, and modern cancer care is becoming far more expensive than traditional hospitalization-based treatment. Long treatment durations, recurring diagnostics, outpatient care, and evolving advanced therapies can create financial pressure that continues for months or even years.

In such situations, payout-heavy structures with higher escalating benefits can feel more aligned with the direction cancer economics is heading. Larger stage-based payouts provide stronger immediate liquidity and greater financial flexibility when treatment costs rise unpredictably.

For younger buyers especially, future-proofing becomes less about choosing the lowest premium today and more about choosing a payout structure capable of handling significantly higher treatment costs in the years ahead, thereby plans like Activ secure will be the choice

Scenario 4: Conservative Buyer Seeking Institutional Trust

Long-Established Institutional Stability of LIC and its Cancer Cover plan or similar plans with long history or reputation of the company is more appealing for conservative individuals and families.

For many Indian households, insurance decisions are not based only on payout structures or treatment flexibility. Trust, familiarity, and perceived long-term stability often play an equally important role.

Conservative buyers, especially middle-class families and older policyholders, may naturally feel more comfortable with institutions that have built decades of public trust and recognition. That psychological reassurance can become important during emotionally uncertain situations like a major illness.

For such buyers, financial predictability, continuity, and confidence in the institution itself may feel more valuable than aggressively structured payout models focused primarily on treatment inflation.

Important Insight : What Buyers should Focus on while Choosing Cancer Insurance

Cancer insurance is not merely about:

- “Which policy is cheaper?”

- or “Which offers higher coverage?”

The real question here is:

What kind of financial damage is most feared?

Different plans protect against different emotional risks.

Some prioritize:

- Aggressive treatment access,

- Immediate liquidity,

- Advanced therapy readiness.

Others prioritize:

- Long-term financial security and continuity,

- Predictable support, and…

- Emotional & financial stability.

Very few policies do both perfectly.

The Harsh Truth About “Enough Coverage”

Even ₹50 lakh may not fully future-proof advanced oncology costs in the coming decade.

Cancer treatment inflation is accelerating rapidly, particularly for targeted therapies and precision

medicine.

That is why:

- Buying early,

- Locking lower premiums, and…

- Choosing meaningful coverage intelligently

matters far more than endlessly postponing decisions.

The younger the buyer, lower the premium and the stronger the long-term financial advantage becomes.

Final Verdict: Which One is Better?

Activ Secure is Better If:

- Aggressive treatment readiness matters most,

- Higher-stage payouts are important,

- Modern therapy access is the priority, and…

- Younger earning years need stronger protection.

LIC Cancer Cover is Better If:

- Long-term financial security and continuity matters more,

- Recurring support feels emotionally important,

- Conservative financial structures feel safer, and…

- Stable monthly income matters deeply.

The Smarter Perspective

This is not truly a decision of:

“Which policy is better?”

It is a decision of:

“Which financial fear deserves protection first?”

That priority changes everything.

Because when cancer enters a household,

It becomes:

- Time,

- Dignity,

- Choice, and

- The ability to stay positive without financial panic.

Must read Cash Shield For Cancer: Why Do You Need It : India’s Urgent Overlooked Lifeline